Dublin VAT Calculator

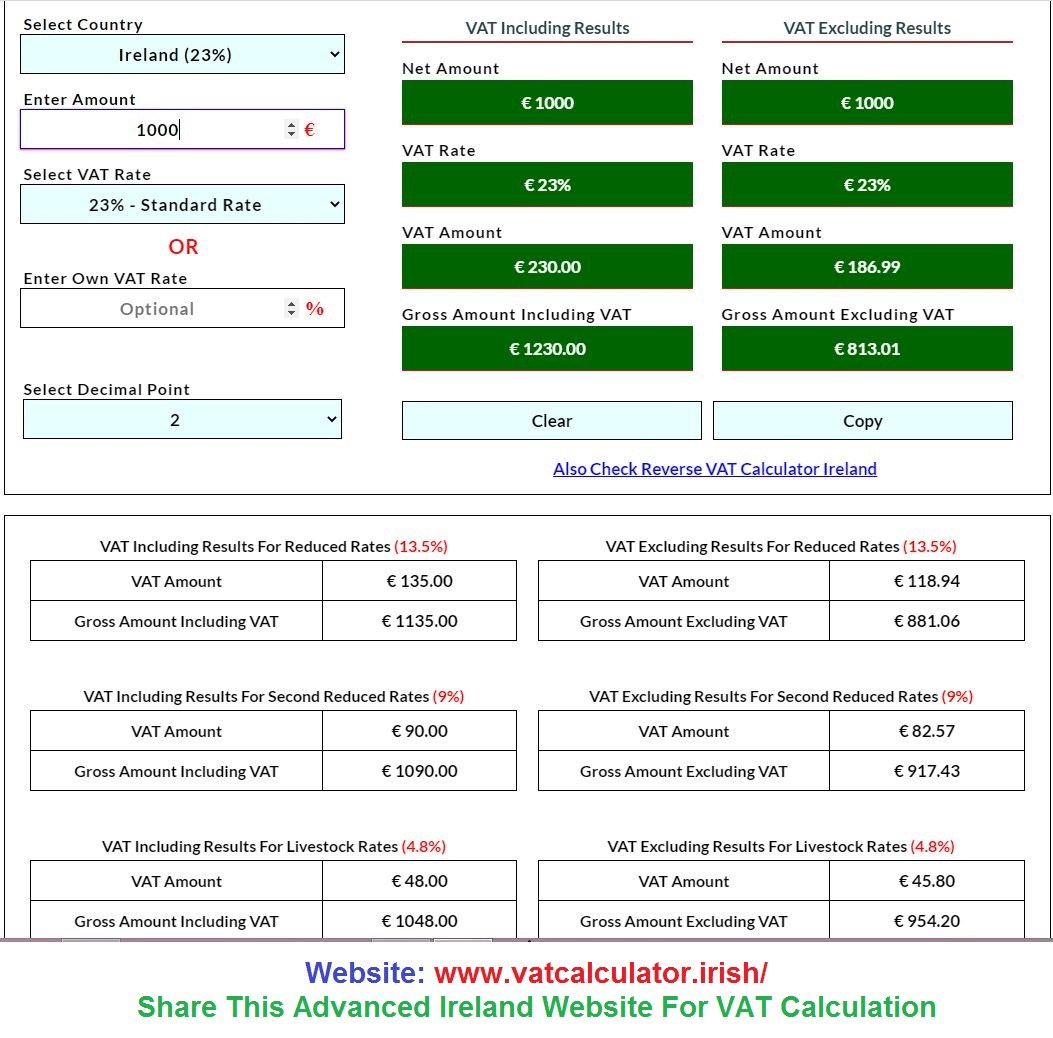

VAT Calculator Dublin – Provides Comfort to Personal Calculation of Taxes The definition of VAT calculators unstated, it is merelydesigned to help businesses and individuals alike quickly compute theiroutput or Value Added Tax on goods based on certain prevailing rates in Ireland. The Irish VAT rates are the same including 23% standard rate, 13.5% reduced rate for some services and a range of zero to lower rates on specific goods in Dublin as they do anywhere in Ireland due to the capital status. It is a process that comes with complexity and confusion, however an VAT calculator allows the users to enter in either net or gross figure so they can view how much the tax amount costs along side complete cost. So if, for example, a company in Dublin wants to work out that’s due on €1,000 worth of services at the standard rate it can quickly be told using this calculator; VAT = 230 making the total $. &nbInterested? This tool is not only vital for correct invoicing but can also support compliances and the accounting process — be it on a minimal scale within small businesses or with larger organizations. VAT calculator in Dublin- Pratical Example Freelancers, small business owners and retailers who must offer fast price quotes or invoices would particularly benefit from a VAT calculator in Dublin. An example of this will be a freelance graphic designer in Dublin, who personally charges €500 per project. If the client is being charged, 23% VAT on top of this net amount (€500) could be input into the VAT calculator in order to establish how much should be invoiced. Which means the VAT would be €100 (20% of €500), in which case, this tool will report that the total amount payable by client is actually around £615. A bit of a back-of-the-envelope calculation, but it lets companies be transparent with customers and collect the right amount of VAT (necessary to comply with tax duties to the Revenue Commissioners in Ireland).

Value Added Tax

Comprehending the Idea of Value Added Tax (VAT)

VAT(Vat is a sort of use charge.) A Value Added Tax (VAT) is an immediate utilization expense. Sales tax is generally charged at the point of final sale to the consumer, whereas VAT is collected incrementally, over a series of transactions in production and distribution (in addition to its ultimate value) — from but not including raw materials / component purchases up through retail.. A simple example: An electronics manufacturer buys raw materials in the amount of $100 and pays a 10% VAT, paying out thus$110. The manufacturer must pay a 10% VAT tax when it sells the finished product to a retailer for $200 + VAT which then combines and equals $220. As a result, the retailer can recover VAT already paid down the chain so that they only effectively pay VAT on their addition to value in relation much the product was worth. This system results in the tax being borne by all entities involved at each stage but refunded to only those paying it last, thus making VAT a valuable source of revenue for governments worldwide.

The VAT Impacted Business and Consumers

VAT affects businesses as well as consumers but the mechanism of how it works for both is different. Businesses will act as a tax collector when they charge VAT on sales, but can reclaim the VAT paid on their purchases (referred to as input tax). This is to lessen the load on businesses; they only serve as middlemen in collecting tax rather than being hung up dry. The VAT is what more consumers are familiar with as it actually built in to the price of goods and services, even though this ramps up before finally reaches the consumer. As an example, if a consumer buys at $1,000 laptop in country with 15% VAT then he or she pays extra of a flat tax= 1000 *. Businesses may deal with the administrative aspects related to Value added tax, however ultimately it is the end consumer that bears such cost and cannot claim a refund of same (which also supports for how VAT generally operates as a consumption-based tax system).

A VAT identification number or VAT identification number This is a number used for Value Added Tax (VAT) purposes in many countries, including European Union member states Within the EU, it is possible to check this VAT ID online on an official website of the European Union: VIES. VAT : VIES: VAT Information Exchange System (checks the validity of a VAT number issued by any Member State ) Ensure the number has been issued, and may hold identifying information such as entity name or other data to differentiate different entities with the same identifier. Nevertheless, VAT identification numbers will often not be available from national authorities due to data protection laws. The full introductory part consists ultimately of the 2-to-13-character country and thus starts with an ISO3166 alpha-2 (two characters) except for Greece, which utilizes EL(ISO6391 language code für Greek) in return or Northern Ireland uses XI to trade within the EU instead. The digits are usually numbers in most countries or letters; they are examples of programmable identification. Foreign firms that offer and source items to consumers and non-enterprise constructs for deals in the EU who exchange under a VAT number starting with "EU" instead of nation codes. Godaddy EU826010755 and Amazon (AWS )EU826009064.

In effect from 1 January 2020: The customer's valid VAT number is mandatory for zero intra-community supplies of goods [EU] Should the customer fail to have a valid VAT number, then we are not able to apply 0% VAT rate. It tells you that a company will make sure the VAT numbers of your customers are accounted for correctly. Make sure your VAT numbers are correct in every country tax system that you correspond with because it is fraud to send ID documents wrongly. The first known example of taxing income in Canada began with a tax that Henry Beeke, the future Dean of Bristol, suggested to Sir Robert Walpole in 1694.

Pitt's income tax was levied from 1799 to 1802, when it was abolished by Henry Addington at the Peace of Amiens. Addington took over as Prime Minister in 1801, following Pitt's resignation over Catholic Emancipation. Income tax was reintroduced by Addington in 1803 when hostilities with France resumed, but was abolished again in 1816, a year after the Battle of Waterloo. Opponents of the tax, who believe it should only be used to finance wars, want all documents relating to the tax destroyed along with its repeal. The document was publicly burned by the Minister of Finance, but a copy was kept in the basement of the tax court.

Residents are generally taxed differently than nonresidents. In some jurisdictions, nonresidents are taxed except for certain types of income earned in the jurisdiction. See, for example, the discussion of U.S. taxation of aliens. However, residents are generally subject to income tax on all worldwide income. A handful of jurisdictions (most notably Singapore and Hong Kong) tax residents only on income earned or remitted to the jurisdiction. There may be situations where a taxpayer has to pay tax in the jurisdiction where he or she is a tax resident and also has to pay tax in another country where he or she is not a resident. This creates a double taxation situation, which requires the assessment of double taxation agreements concluded by jurisdictions where the taxpayer is assessed as resident and non-resident for the same transaction.

Residency is often defined for an individual as presence in the jurisdiction for more than 183 days. Most jurisdictions base the location of an entity on the location of its organization or place of administration and control. Definition of income

Most systems define taxable income generally for residents.

{kind=link}